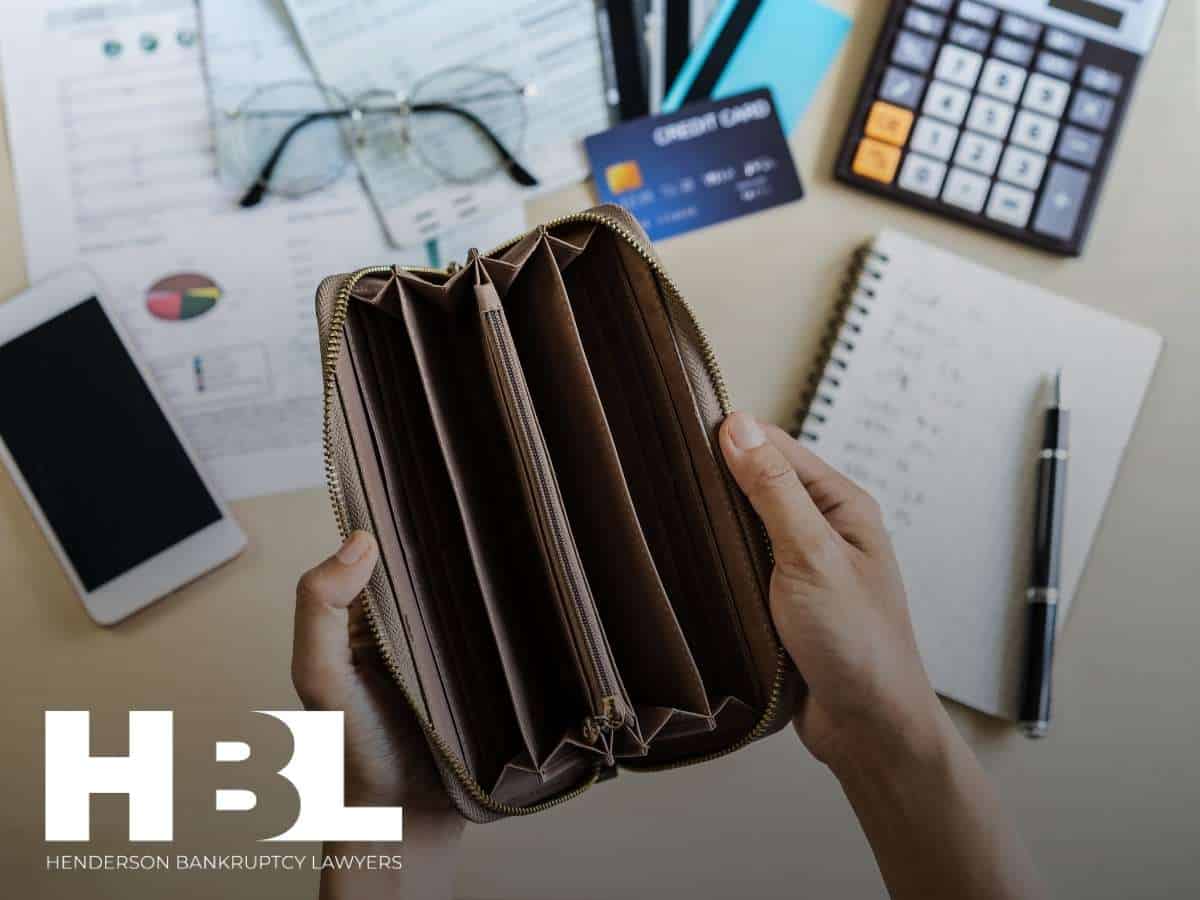

While it seemed like 2020 was the most difficult year the world would seem in a while, it seems like life continues to get more difficult. One of the things making life so difficult for the general population is financial stress- an estimated 64% of American families currently live paycheck to paycheck. That means that unexpected expenses can create serious consequences for families of all configurations in Nevada. Falling behind on rent could mean an eviction and fall behind on a mortgage can mean foreclosure. If your vehicle is financed, your lender won’t give you long to catch up before repossessing the vehicle. Your creditors can even get permission from the court to automatically deduct 25% or more of your paychecks. But bankruptcy may be a way to hold off your creditors and get your financial situation under control. Read on to learn more about the leading causes of bankruptcy in Nevada for 2022. If you would like to schedule a free bankruptcy consultation with Henderson Bankruptcy Lawyers, call 702-370-0155.

Medical Bills

Medical bills are frequently cited as one of the leading causes of bankruptcy not just in Nevada, but in the United States in general. It is estimated that 530,000 American families file bankruptcy each year due to medical debt. That’s why if you’ve begun researching bankruptcy yourself, you may have come across the term “medical bankruptcy.” Medical bankruptcy is the informal term for bankruptcy filed due to medical debts. We say it’s informal because you can’t pick and choose which debts are included in your bankruptcy- if you file bankruptcy due to medical debt, the rest of your debts will be included just the same. This even includes debts to friends and family members.

Just because you have medical debt doesn’t mean you should necessarily file for bankruptcy. Medical providers tend to be more forgiving creditors than credit card companies, auto lenders, mortgage companies, etc. Many hospitals offer bill forgiveness programs based on income level. Medical providers often are also willing to work out payment plans with patients. Additionally, some doctors will fire you as a patient if you discharge their bills in bankruptcy. Talk to a bankruptcy attorney about whether a medical bankruptcy is right for you by calling 702-370-0155.

Divorce

Divorce can completely upend someone’s life in every single way. One of the most crucial factors that divorce can impact is someone’s budget. A divorcee could be forced out of their marital home, and even still be financially liable for it. Unless they have someone else to move in with, they will have living expenses for their new residence, and could even have to pay spousal maintenance and child support. Property division could also result in being ordered to pay a disproportionate amount of marital debt.

Filing bankruptcy after divorce doesn’t come without its complications. You could still be held liable for community property debts you discharge, depending on the terms of your property division orders with your ex. Talk to a Nevada bankruptcy attorney for more information at 702-370-0155.

Loss of Job or Income

It’s not hard to imagine how losing your job, or any other source of income could cause someone to fall into debt and eventually declare bankruptcy. Unemployment of even a few weeks could mean failing to pay bills or relying on credit cards to make ends meet. This hole can be hard to get out of even after finding a new job. Payday lenders and other predatory lines of credit will take advantage of desperate times to charge astronomical interest rates. If someone uses these lines of credit and fails to pay them back timely, they can expect steep interest payments, and possibly a wage garnishment in the future.

Inflation

The cost of just about everything has been increasing faster than usual as of late. When the prices of necessities like gas and groceries increase, it leaves the average family with less wiggle room for unexpected financial emergencies. Although the Inflation Reduction Act was signed in 2022, costs are increasing for Nevada families faster than their incomes can keep up. Bankruptcy may not be able to increase someone’s income, but it can potentially increase a debtor’s disposable monthly income. What does this mean? Let’s say a family purchased an expensive vehicle with financing a few years ago. One spouse lost their job, retired, or for some other reason, they can no longer afford the vehicle. Rather than wait for the vehicle to be repossessed, take the hit to their credit, and possibly be left with a repossession deficiency after the vehicle is sold at auction, the family can surrender the vehicle and its attached debt in bankruptcy.

COVID-19

While most of the protections put into effect in 2020 due to the pandemic have ended, many people are still experiencing the financial impact of COVID-19. It caused widespread unemployment, with Nevada experiencing the highest unemployment rate in the United States. A large part of our economy relies on tourism and entertainment, which was put at a near standstill at the height of the pandemic. Even after businesses that were forced to close due to pandemic restrictions reopened, employees and business owners alike still see reduced income.

Some businesses that saw losses from the pandemic still haven’t reached levels from pre-2020. With expenses increasing from inflation, families have less disposable income available for a lot of what Nevada has to offer. While Chapter 13 bankruptcy isn’t available for most business owners, Chapter 7 can help a small business owner struggling with debts. When that isn’t appropriate, there are also small business provisions for Chapter 11 bankruptcy.

How To Utilize an Emergency Bankruptcy Filing in Nevada

If your vehicle is about to be repossessed, your home is about to be foreclosed, your wages are about to be garnished, your utilities are about to be shut off, or one of your creditors filed a lawsuit against you, this can be considered an “emergency” situation when it comes to bankruptcy. This is because the petition needs to be filed quickly so that the debtor can be protected by the automatic stay as soon as possible. The automatic stay prevents all the types of creditor collections listed above and more. Bankruptcy courts allow debtors under these types of circumstances to file an emergency bankruptcy, also known as a “skeleton petition.”

There are several types of documents you will need to prepare your Nevada bankruptcy petition. These can take time to gather, and that is time you probably don’t have in an emergency. Fortunately, you will only need a few of these documents to file a skeleton petition and activate the automatic stay. You need to be able to prove your income level with your skeleton petition, meaning you will need six months of proof of income. It’s also necessary that you complete the first online credit counseling course before filing a skeleton petition so that you can provide your course completion certificate as well. You will need to have a list of your creditors for your creditor mailing matrix. This can usually be assembled using your credit report. Talk to your bankruptcy attorney about any other documents they require to file a skeleton petition on your behalf.

After filing a skeleton petition with the bankruptcy court, the debtor has two weeks to assemble and file the rest of their petition. If this is done correctly, the bankruptcy will then proceed as usual. The debtor will receive a letter from the trustee that usually contains requests for documents and will include the debtor’s scheduled 341 Meeting of Creditors information. The 341 Meeting of Creditors is meant to verify the debtor’s identity, work out any issues with the petition, and allow creditors the chance to object to their debts being discharged. The debtor also needs to complete a second online credit counseling course and file the course completion certificate with the court within 60 days of the 341 Meeting of Creditors.

If you need to file for bankruptcy in Nevada quickly, our office may be able to help. Call 702-370-0155 or click here to schedule your free consultation.

Nevada Bankruptcy Lawyers for Your Situation’s Needs

Filing bankruptcy self-represented is cheaper but opens you to risks and pitfalls that a bankruptcy attorney can help you identify and avoid. No matter what reason you are considering bankruptcy, our lawyers can offer an understanding ear and knowledgeable information about the bankruptcy process. Henderson Bankruptcy Lawyers offers affordable quotes for representation with payment plans starting at ZERO DOLLARS DOWN. To learn more, contact us or schedule your free consultation at 702-370-0155.

![]()

Henderson Bankruptcy Attorneys

1489 W. Warm Springs Rd., Ste. 110

Henderson, NV 89014

Phone: (702) 899-3328

Email: [email protected]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}