Best Ways to Avoid Bankruptcy When Unemployed

It’s no secret that the coronavirus pandemic has left millions of Americans unemployed. Now that the extra $600 weekly unemployment benefits provided by the Coronavirus Aid, Relief and Economic Security (CARES) Act have expired, many families will now have to rely on lines of credit to make ends meet. There was a 33% increase in bankruptcy filings during the recession of 2008, and economists expect to see a similar spike in bankruptcies due to the pandemic. Bankruptcy is intended to be a last resort for debtors, so there are steps you can take to avoid it if you are struggling financially because of COVID-19.

It’s no secret that the coronavirus pandemic has left millions of Americans unemployed. Now that the extra $600 weekly unemployment benefits provided by the Coronavirus Aid, Relief and Economic Security (CARES) Act have expired, many families will now have to rely on lines of credit to make ends meet. There was a 33% increase in bankruptcy filings during the recession of 2008, and economists expect to see a similar spike in bankruptcies due to the pandemic. Bankruptcy is intended to be a last resort for debtors, so there are steps you can take to avoid it if you are struggling financially because of COVID-19.

Tips to Avoid Bankruptcy in Las Vegas

- Communicate with your creditors: You are not the only person struggling to keep up with bills, and your creditors may already have policies in place to address collecting debts during a time of mass unemployment. Your creditors may be willing to defer your payments, which can help you avoid negative marks on your credit, or lower your interest rate.

- Become a bargain shopper: Take advantages of sales and store membership benefits. Use your credit card points. Give homemade gifts or gifts of service instead of buying expensive presents. Shop at warehouse stores for essential supplies.

- Be a mindful driver: Gas stations often give a discount if you pay at the register with cash instead of using a credit card at the pump. Avoid gas stations near the freeways as they usually charge more. Check your tire pressure and conduct other maintenance on your car regularly so you get as much mileage as possible.

- Seek out financial assistance: You may have family or friends who are willing to help you out. There are also many local organizations that can help you with things like paying rent and keeping food on the table.

Nevada’s Unemployment Crisis

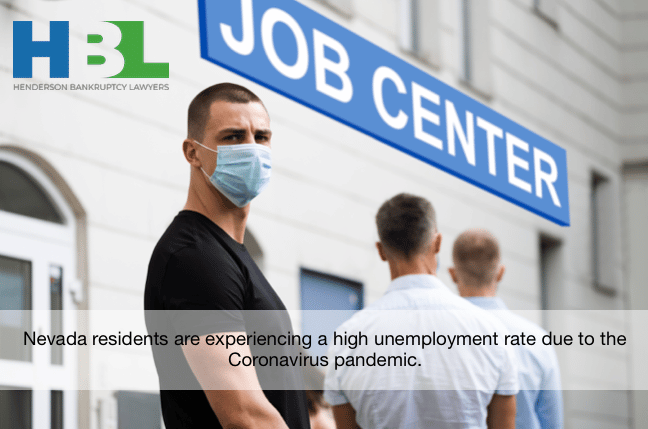

Nevada has been hit especially hard by the pandemic, in part due to how many Las Vegas residents work in the entertainment industry and other nonessential businesses that have been forced to close the past few months. In April 2020, Nevada saw its peak unemployment rate- a shocking 30.9 percent. The unemployment crisis nationwide has been compared to the Great Depression, but even then the unemployment rate only reached 24.9 percent. On average, Nevadans who were receiving the extra $600 weekly unemployment benefit briefly had higher income than before the pandemic.

Nevada has been hit especially hard by the pandemic, in part due to how many Las Vegas residents work in the entertainment industry and other nonessential businesses that have been forced to close the past few months. In April 2020, Nevada saw its peak unemployment rate- a shocking 30.9 percent. The unemployment crisis nationwide has been compared to the Great Depression, but even then the unemployment rate only reached 24.9 percent. On average, Nevadans who were receiving the extra $600 weekly unemployment benefit briefly had higher income than before the pandemic.

Can I File Bankruptcy without Money? I am Unemployed.

This depends on which Chapter of bankruptcy you want to file. Most individual bankruptcies are either filed as a Chapter 7 or a Chapter 13. Filing Chapter 13 bankruptcy will be difficult if you are unemployed. A Chapter 13 bankruptcy is a payment plan for your debts that lasts 3 or 5 years. Your monthly payments will be based on your average monthly income, how much of it is disposable, and the amount and types of debts you have. Some types of debts need to be paid in full in the plan, like past-due child and spousal support and arrearages on your mortgage or auto loan for an asset you wish to keep. If you are unemployed, you likely won’t have enough income to pay at least the minimal required debts, and your case would be dismissed.

On the other hand, being unemployed will actually help you qualify for a Chapter 7 bankruptcy. While you need to have enough income to make payments in Chapter 13, you need to have low enough income to excuse you from paying your debts in Chapter 7. Debts are liquidated without repayment in Chapter 7, so it can only be available to those that really need it.

There are two ways to qualify for a Chapter 7 bankruptcy. The first way is to make less than your state’s median income. For a single-person household, this amount is $52,449 per year, or $4,370.75 per month. If you are married or have a child under the age of 18, this amount increases to $65,756 per year or $5,479.67 per month. However, if your spouse is employed, you will need to need to be under the state median combined. The median raises to $74,856 per year or $6,238 per month for a family of three, $81,528 per year or $6,794 per month for a family of four, and so on. Your income will be calculated using your average income over the past 6 months. Therefore, the longer you stay unemployed, the better chance you have of meeting your state’s income requirement.

The second way to qualify for a Chapter 7 bankruptcy is through the Means Test. The Means Test will take your average monthly income over the last six months less mandatory deductions, certain tax and student loan payments, etc. The number you reach is referred to as your disposable monthly income. If your disposable monthly income is negative, or below a certain amount that is based on your state and family size, you will be eligible to file Chapter 7. Be careful if you use this method to qualify, as mistakes on the Means Test could result in your case being dismissed. Either way, a few months of unemployment should help you qualify for Chapter 7 through both methods.

I Qualify for Bankruptcy. How Do I Pay for my Bankruptcy in Las Vegas, Nevada

Qualifying for bankruptcy is great, but you’re probably now wondering how you will actually pay for your bankruptcy. The filing fee for a Chapter 7 is $335, and attorney’s fees are typically considerably higher. Most Las Vegas Bankruptcy attorneys will require you to pay both of these in full before your petition is filed. That’s why attorney Erik Severino has chosen to offer the option of post-filing payment plans to his Chapter 7 clients. Clients who qualify can file their case with NO money down and make affordable monthly payments for 12 months after filing at a 0% interest rate.

If you are considering bankruptcy, know that you aren’t alone. If half as many file bankruptcy as are expected to because of the pandemic, the stigma surrounding declaring bankruptcy will surely decrease. If you have more questions about qualifying for bankruptcy or our post-filing payment plans, call today to schedule your free consultation. Call (702) 899-3328.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}